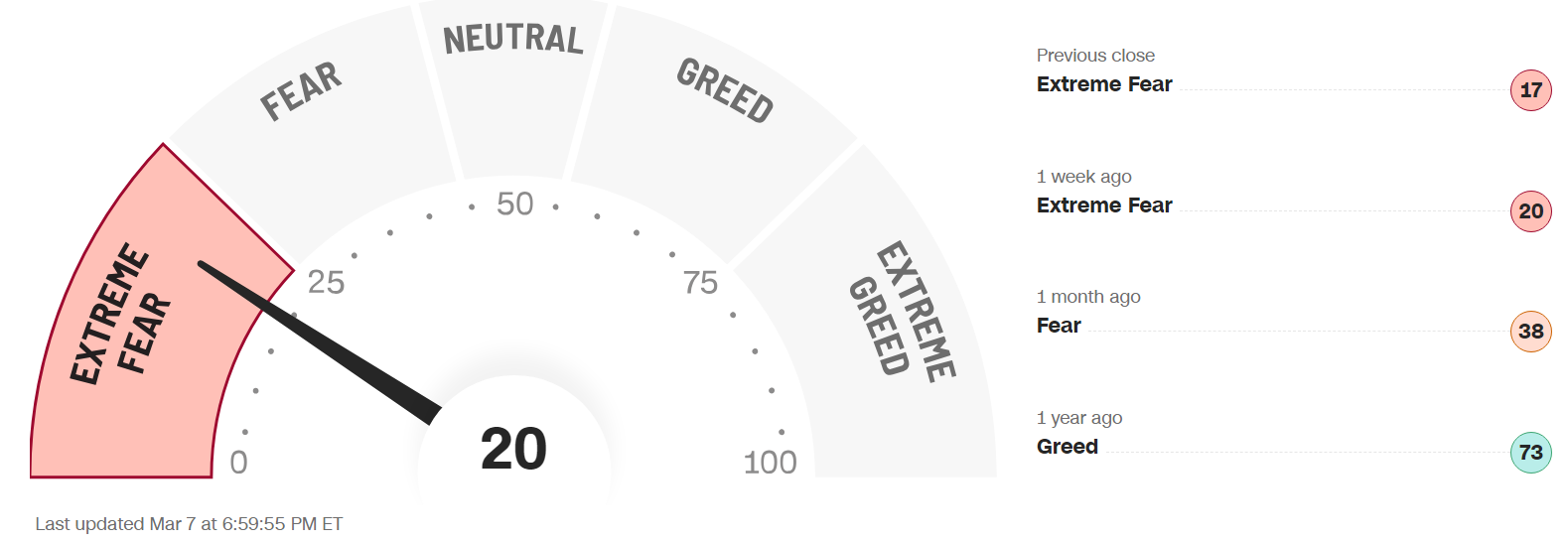

FEAR & GREED INDEX 20

The Fear & Greed Index (found on cnn.com) is one of the easiest indicators to use to determine current market emotion. This simple to read gauge, highlighted in our publication When to Buy and When to Sell: Combining Easy Indicators, Charts, and Financial Astrology (available on Amazon), is measured in a range from 0-100, and currently reads 20 as of the close on Friday, March 7, 2025.

This figure remains in the Extreme Fear level, where it entered last week, as it again closed with and equal reading of 20, after another late Friday rally. As we focus on in our publication and weekly blogs, the markets usually react quickly to extreme conditions. This week, the S&P 500 did not make it out of the extreme fear level, but did close positive on two of the last three days. The index itself fell about 186 points from 5,954 to 5,770, a decline of about 1.5%, to its lowest level since early November. Remember, the major indexes are only a couple of weeks removed from All-Time Highs, though the Russell 2000 small cap index is clearly in a bear market. The S&P and Nasdaq are also bordering bear market territory, while the Dow Jones Industrial Average remains above.

The “Risk-Off” sentiment generally remained, including cryptocurrencies, as a Crypto Summit on Friday did not yet settle the ongoing saga of whether the United States will actually purchase Bitcoin to keep in reserve. 10-year bonds dropped slightly, with yields rising from 4.2%, to 4.3%, as the U.S. Dollar continued to weaken.

The 7 internal factors used to formulate this index are listed on the screen (below):

Market Momentum – (S&P 500 vs its 125-day moving avg) = EXTREME FEAR

Market Volatility (measured by the VIX) = EXTREME FEAR

Put to Call Ratio 5-day avg. (# of Puts (bearish) vs Calls (bullish) = EXTREME FEAR

Stock Price Strength (# of new 52-week highs vs new 52-week lows) = EXTREME FEAR

Stock Price Breadth (# of shares rising vs falling on NYSE) = EXTREME FEAR

Safe-Haven Demand (which measures stocks vs bonds) = EXTREME FEAR

Junk Bond Demand (non-govt. bond yield spread) = EXTREME GREED

This week, 3 of the 7 factors changed levels, and 6 of the 7 have fallen to the Extreme Fear level, as the markets continued to sell off most of the week until late Friday. Last week we noted that it was interesting that the PCR was late to the party, but had finally succumbed to the pressure. This week, the VIX finally fell into this category, after spiking to its highest level since December. As we also warned for several weeks, stock selection was key with the weak underlying conditions.

As noted, the VIX, measured by Market Volatility, increased significantly this week. Overall, it rose 3.7 points, or 19%, settling in at 23.3, from 19.6 (pulling back slightly on Friday), entering the Extreme Fear territory amid investor nervousness and uncertainty. Both the Fear & Greed Index, together with the VIX, at these levels, suggest most of the current selling could be over. Although there is no set time frame for recoveries, the more extreme the level, the faster a likely price reversal.

This week’s negative economic news included continued weak retail earnings, slowing growth, reduced home construction and sales, and the Atlanta Fed’s forecast of a major plunge in GDP this year. The favorable news included steady jobs numbers (unless later revised), and slightly higher factory orders. The bad news generally outweighed the good, continuing the negative sentiment, further supporting our theory that emotion is the main driving factor of short-term market moves.

Astrologically, the planet Mars continues its aggressiveness energies in the sign of Cancer (until April), symbolizing the “protection of the home,” which has been evident by the new administration’s determination to secure and protect the country over the past month and a half. As noted, cybersecurity companies continued to show strength following strong earnings reports. The threat of global conflict remains under this aspect as well, as we have also discussed in recent blogs. Many “hidden truths” and “deceptive practices” continue to be uncovered, especially related to government and money (signified by Neptune and Saturn in Pisces). Pluto in Aquarius themes, which favors the “people,” over “government” controls, (discussed in previous Trader Transit, Planet Power, and weekly blogs), also continue as divisive demonstrations and protests have not subsided.

As we pass through Pisces season, which symbolizes confusing, delusionary, and theatrical Pisces energies (please review our Sign Language – Pisces blog, dated 2-5-25), the volatility continues with the unknown and uncertainty of global financial conditions. As previously discussed, these energies recently replaced the “free and liberating” theme of the sign of Aquarius, and have been on full display with the discovery, and reaction, to the wasteful government spending findings. We also warned that February is historically the 2nd weakest month for equities, especially the 2nd half, which encompasses the beginning of Pisces season. As expected, the volatility and uncertainty increased, and resulted in universal price dips.

The recently discussed Venus Retrograde started last weekend, in the sign of Aries (ruled by Mars), symbolizing continued aggressive (Mars) financial (Venus) energies. The associated likelihood of a market pullback began a few days prior (known as an “orb” or “shadow period”), and carried through the first week of this phenomenon (please review our recent Planet Power - Venus Retrograde blog, dated 2-17-25, for more details). Aries is often associated with fast beginnings, that quickly fade, so continue to be aware of potential “false breakouts,” and short-term reversals. During this retrograde, Venus will temporarily return to Pisces (from March 29 to April 16), again mixing these opposite energies.

As noted, the planet Mercury also turns retrograde this coming Friday, March 14 (lasting through April 7), while also in the sign of Aries. Mercury retrograde often results in volatility and/or multiple price reversals, signifying mixed communications. As both planets will move back and forth between Pisces and Aries during their retrogrades, it is likely to jumble the energies of both signs, further distorting the clarity of the markets. Last week, Mercury ran into Saturn (restriction), for a brief conjunction, which resulted in an about face in the equity markets on Monday and Tuesday. Mercury is now conjunct with Venus (love and money) this weekend (and will be again on March 28), with the combined current energies suggesting continued volatility. Expect more tumultuous price action with this active sky, together with all the personal planets’ changes of direction. Reducing share size on holdings and/or trades might be a consideration for those with a shorter-term investment time frame. Be especially cautious of “false breakouts” during this activity.

Look for sectors such as financials, defense, pharmaceutical, communications, technology, gold/silver, and cryptocurrencies to continue to be in focus, again with likely volatility and a possible bounce (based on the current Fear & Greed level). In the longer term, certain subsectors of the technology industry are likely to continue their advance into the future, including AI, robotics, quantum computing, and space development (with Pluto in Aquarius, and Uranus upcoming ingress to Gemini in mid-2025).

Gold (ruled by the Sun), and Silver (ruled by the Moon), rose, dipped, then leveled out by weeks end, despite the weak dollar, after pulling back from recent all-time highs. As we noted the last two weeks, the bullish cycle is getting rather old, supporting a pullback or consolidation. Mars’ transit through Cancer, which resulted in gains on the previous occasion (from early September to early November of 2024), continues through early April. As we have expressed, any pullback in these metals will likely be short-lived (as long as the dollar remains weak) and they continue to be long-term buying opportunities on any declines. The Gold to Silver Ratio (covered in our publication) dropped slightly by weeks end, from 91.7 to 89.5, indicating the two metals are closer to equal value.

***As always, this information is not intended to be financial advice, or any specific buy or sell recommendation, but rather a guide to assist the reader in some further understanding of current economic conditions/movements in the sky, and how they can affect moods, behaviors, world events, and financial markets.