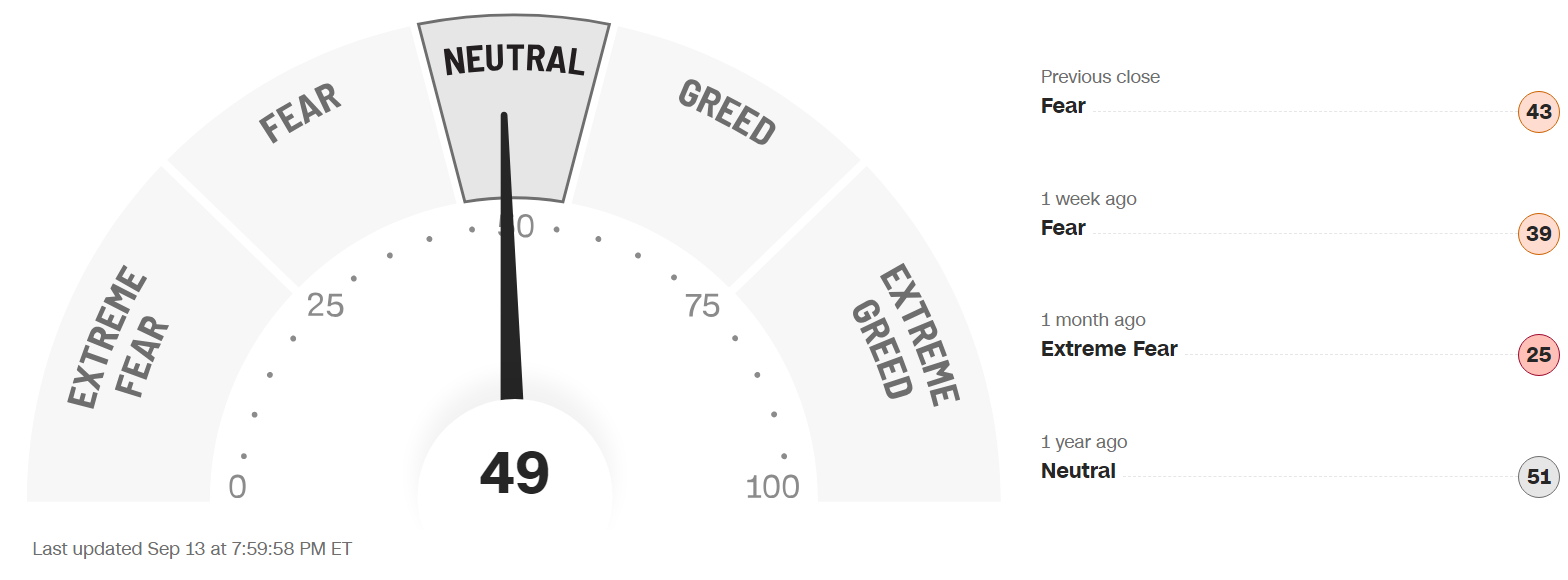

FEAR & GREED INDEX 49

The Fear & Greed Index (found on cnn.com) is one of the easiest indicators to use to determine current market emotion. This simple to read gauge, highlighted in our publication When to Buy and When to Sell: Combining Easy Indicators, Charts, and Financial Astrology - available on Amazon, is measured in a range from 0-100, and currently reads 49 as of the close on Friday, September 13, 2024.

This figure moved into the mid-Neutral level, from the Fear level from the end of last week, with a sudden reversal to start the week, and again during the mid-day hours on Wednesday, increasing 10 points from last Friday’s close at 39, a move of slightly more than 25%. This was supported by an increase of 118 points in the S&P 500, from 5,508 to 5,626, a rise of just over 2%, from the beginning of the week to the end. The move brings the index back to almost equal to its closing two weeks ago at the end of August. The 3 major U.S. Indexes (Dow Jones Industrial Average, S&P 500, and Nasdaq) all moved in tandem, including the sudden dip and reversal on Wednesday, suggesting less fragmented markets after weeks of “divergence”.

The “Risk-on” theme continued (despite the Wednesday activity) as the expectation of a rate cut at the September 18 FOMC meeting continued, despite weak economic reports. 10-year bond yields continued to fall from the 3.7% range, to about 3.6%, below 4% for the 6th straight week. Falling rates normally assist a weak economy, but also usually leads to higher inflation. As also noted, the last few weeks, the recent steady decline in the 10-year is also evidence that the Fed already started cutting rates behind the scenes, as there are indications that they are also simultaneously buying the debt (bonds/treasuries) themselves. Bond funds, including TLT, surged at the beginning of the week, but leveled off by weeks end. Should the Fed begin to cut rates aggressively, look for treasuries and bond funds to further increase. Further drops in oil prices (though it rose slightly at weeks end), manufacturing and production, and high rates of unemployment and personal debt, continue to indicate a fragile economy.

This week’s economic reports did not change the overall negative sentiment, with most falling in-line or with a slightly negative bias. This included jobless claims, Core inflation, and consumer and producer pricing, which suggests a rate cate cut may not be the best course of action (which has now been “price-in” to the market). Consumer sentiment did rise slightly as well, confirming the same. The real estate industry also continues to struggle, contrary to major real estate companies reporting the opposite (please see yesterday’s Real Estate - Deception blog, dated 9-14-24, for more details).

Nvidia (NVDA) remained in the news again this week, after earnings 2 weeks ago and rumors of a DOJ subpoena last week (that was later denied), that caused the largest 1-day loss of market cap in the history of the stock market. This week, Nvidia’s CEO Jensen Huang announced that the future remains bright with the company regarding its AI division, sparking new life into the stock price on Wednesday and Thursday. The chip industry remains weak despite this week’s rise, so continue to be cautious with new investments in this sector.

The 7 internal factors regarding this index are listed below, with their current readings:

Market Momentum – (S&P 500 vs its 125-day moving avg) = GREED

Market Volatility (measured by the VIX) = NEUTRAL

Put to Call Ratio 5-day avg. (# of Puts (bearish) vs Calls (bullish) = FEAR

Stock Price Strength (# of new 52-week highs vs new 52-week lows) = EXTREME GREED

Stock Price Breadth (# of shares rising vs falling on NYSE) = GREED

Safe-Haven Demand (which measures stocks vs bonds) = FEAR

Junk Bond Demand (non-govt. bond yield spread) = EXTREME FEAR

Four of the seven factors changed levels this week, led by Market Momentum, which returned to the Greed level, after falling to the Fear level last week. The Put to Call Ratio steadily rose throughout the week as well, and now sits at 0.81, at the Extreme Fear level (after reading Neutral just last week), its highest reading since the early August market dip. This also symbolizes the growing “fear” in equities, as there are more open Puts (negative bias) than Calls (positive bias) than previous weeks in the options markets.

The VIX, measured by Market Volatility, remains in Neutral territory, decreasing from last week’s close of 22.3, to 16.5, a drop to “normal” levels after last week’s rise. As noted the past few weeks, the 7 indicators continue to display uneven levels, consistent with our previous reports of seasonal weakness in the month of September. Continue to be cautious with new investments until a new uptrend is confirmed.

Astrologically, as noted last week, the Uranus Retrograde, which began on Tuesday, September 3, immediately resulted in a violent, sudden, trend reversal in technology stocks, typical of Uranus (the “disruptor”), as it represents the tech sector. Another apparent trend reversal occurred mid-day this Wednesday, with no real catalyst. Remember that this retrograde will not end until January 30, 2025, and will also encompass the next Mercury retrograde from November 25 thru December 15, 2024, so be prepared. Mercury also formed another square (challenging aspect) with Uranus (sudden, unexpected change) last weekend, as it did on August 18, which resulted in a continuation of short-term changes of direction in the technology sector. This has now occurred on several occasions, including earlier this week. Mercury also just entered one its two “home” signs, Virgo, further signifying volatility.

The Jupiter/Saturn square (see our Trader Transits -Jupiter Transits blog, dated 8-1-24) continues, and several Venus (money) aspects remain in effect (again, see our recent Trader Transits – Venus in Libra blog, dated 8-21-24), which tend to associate with short-term price action. Venus is now positioned in the sign of Libra (Aug 29 – Sep 22), before moving into the sign of Scorpio.

The planet Mars has also now settled into the sign of Cancer (Sept 4), which is the Ascendant/Rising sign of the U.S. Stock Market (see previous USSM blogs). As we often discuss, the Mars planet energies are very aggressive and determined, suggesting strong moves in price and sectors, as Cancer is very emotional. Be careful not to get caught up in FOMO (over-exuberance) or FUD (panic). The defense/military/homeland sector remains a focus during this time frame. Mars in Cancer has just recently coincided with a sharp rise in leading cybersecurity stocks (defending the “home”), as discussed in previous blogs.

As we continue to navigate through the last week of Virgo season (August 23 – September 22, see our Sign Language – Virgo blog dated 8-8-24), the uneven price movements are expected to remain. Remember that September is historically the worst performing month of the year, and a continued sustained rally at this time would be surprising (but you never know with the strong Uranus energies). Market sentiment normally remains skittish during this time frame, even without these added short-term geo-cosmic energies. This week’s lunar eclipse in Pisces on Tuesday/Wednesday may also affect markets without any substantial publicized reason.

As mentioned during the past few weeks, continue to keep an eye on sectors including consumer staples (necessities), defense, real estate, and healthcare (on the upside), and consumer discretionary (luxury), retail, and energy (on the downside), should economic reports (and revisions) continue to be weak. Recession conditions will also hit those sectors hard, in addition to the transportation industry, including airlines, oil, and transports.

Gold (ruled by the Sun), and Silver (ruled by the Moon), continued their move up again late this week, and as consistently noted, remain buying opportunities on any pullbacks. The general premise is that when the dollar weakens, commodities will rise, especially these metals, as they are considered a hedge or “safe haven.” The fact that the Fed appears closer and closer to rate cuts suggests further potential gains in these metals, though a severe recession would weigh on all sectors. Remember that ETFs which track gold (such as GLD), and silver (such as SLV) can be used to trade the market, as an alternative to holding the physical metal. Cryptocurrencies may also become active again due to the Venus position in Libra, and the ensuing Libra “season” beginning on September 23.

***Full Disclosure: We currently hold a bullish position in SLV, since December of 2023.

***As always, this information is not intended to be financial advice, or any specific buy or sell recommendation, but rather a guide to assist the reader in some further understanding of current economic conditions/movements in the sky, and how they can affect moods, behaviors, world events, and financial markets.